Using construction audit and review techniques to evaluate and mitigate project risk

Whether or not your organization has an internal audit function, the use of construction audit and review techniques is critical in mitigating enterprise risk for large construction projects. Your efforts in assembling a construction compliance review team, no matter its size, may yield some project cost savings as well. The next time your organization undertakes the construction of a new school, wastewater treatment plant or public safety building, consider using some of the following techniques to help ensure yourself and management that effective spend and allocation of resources has been made. Establishing a robust internal control process over facility construction can offer risk mitigation and positive results no matter the size or spend of construction activities.

Building credibility

During a review of construction activities, it is important to create a collaborative environment among the internal audit or compliance professionals. In order to do so, it is necessary to build knowledge of the construction process. Your team needs to learn to speak the language of construction and contractors. Without this knowledge, your team will be unable to ask probing questions to senior leaders, construction project managers and personnel to determine proper application of controls or areas for further review.

Which approach is most effective?

Consider how your team will deploy their review. Will they be involved from the beginning of a construction project? Will the construction review be made an integral part of the construction activities? Or will the review be part of the project close prior to final payments or release of retainages? Each approach will provide value, however, having construction compliance professionals involved from project initiation will instill a spirit of “trust but verify” to the overall project. This may lead to more compliant behavior by contractors without impeding project progress. On the other hand, only involving your compliance team in the project close process may slow final pays to contractors due to the time investment of data gathering and review.

The discussion for the remainder of this article is from the perspective that your compliance team is part of the construction project from project initiation to completion.

Risk assessment and creating a collaborative environment

To ensure high-level risks are mitigated, the first step in the construction audit process is to perform a risk assessment of the common risk areas in a construction project. Confirm you are covered in these five common areas:

- Contract term definitions are understood by all parties

- Records are accessible to review for compliance

- Costs charged are within the scope of the construction contract

- The contractor has the financial strength to pay subcontractors and finance its financial and operational construction requirements

- What has been promised in the contract is delivered

In addition, some questions to ask in the project planning phase to help mitigate risks may include:

- Are key terms (e.g., “substantial completion”) defined?

- Have allowable and non-allowable costs been specified?

- Does the contract have provisions for review of supporting documentation (e.g., subcontractor invoices, time records, payroll burden calculations, etc.) and other record access?

- Are delivery timelines specific?

- Are contract pay rate schedules and fee calculation formulas detailed and unambiguous?

- How does the financial stress test of the prime contractor look?

Time should be budgeted by the compliance project team to participate in ongoing construction operational meetings. Expectations should be set for how the compliance team will provide feedback to your organization’s construction project manager and the contractor. Agreed upon protocols should also be established.

Audit the first pay application

One effective practice Baker Tilly has found is auditing the first pay application to:

- Verify arithmetic accuracy

- Confirm pay rates and burden calculations

- Compare amounts billed on the pay request to supporting documentation for labor and equipment

This activity, while it is basic auditing, does serve to put the prime contractor on notice that areas will be reviewed and the contractor’s documentation needs to support amounts requested, thus setting the stage for future pay request documentation.

Where are the key internal controls in the process?

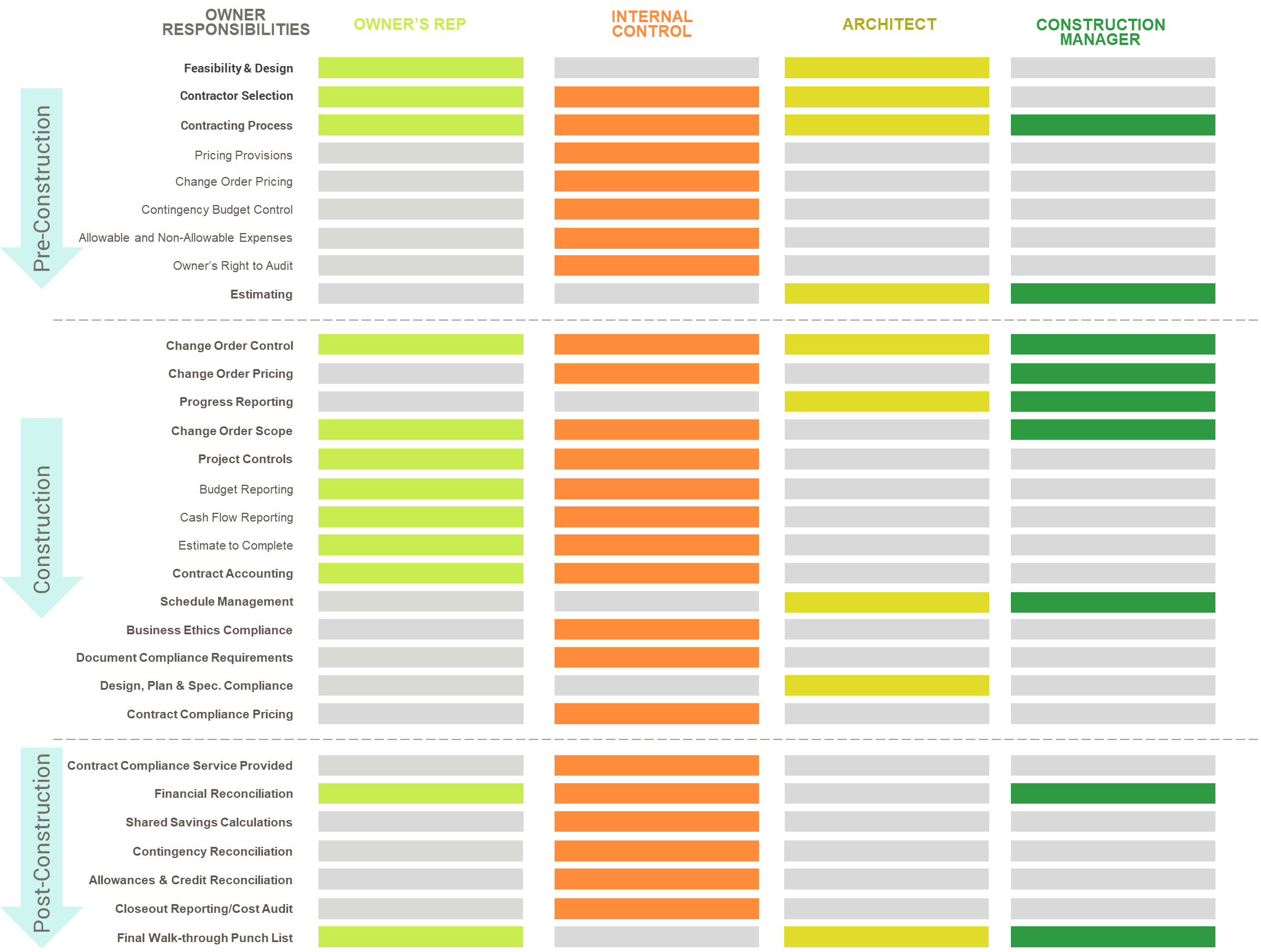

Any major construction project involves four main participants:

- Owner’s representative (rep) or your organization’s project manager

- Internal controls owner

- Architect or project designer

- Construction manager or general contractor

The common roles and responsibilities of each are shown in the following chart:

While duties by position vary throughout the project depending on the project activities, the internal control review function permeates almost each step of the process. All of the controls on the chart above are designed to mitigate or address a key project construction risk. This process of continuous monitoring is the most involved and will yield the highest level of results, providing management comfort that project risk is being analyzed, documented, tested and reported.

Managing expectations

The industry rule of thumb is to budget audit hours of 0.001% times the construction project cost. For example, a $50 million project should have 500 audit hours.

The cost of the construction audit is a capitalized project cost, similar to the cost incurred for project management, engineering services and construction materials. There are various funding options available to help with the incurred cost of a construction audit, including:

- Capitalizing the cost with other construction costs

- Charging back the costs to facilities management

- Including the cost in the annual internal audit budget

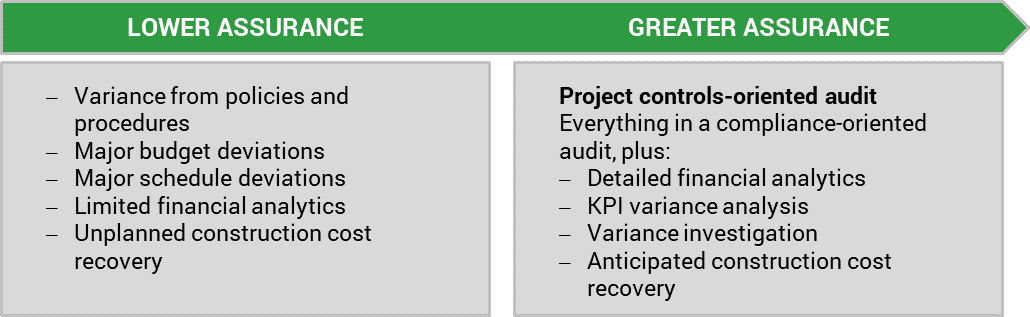

Utilizing a compliance team as part of the construction audit process will provide greater assurance, comfort and risk mitigation over large construction projects. In the continuum scale, greater use of construction audit techniques will provide greater assurance that the cost side of the equation has stronger controls and those controls are being leveraged for your organization’s benefit.

Whether your organization makes use of internal audit resources, assembles a group of individuals from within the organization or outsources these services to a construction audit specialist, you should expect positive results.

For more information or to learn how Baker Tilly can help, contact our team.